Performance and Portfolio Activity

For the professional adviser community only

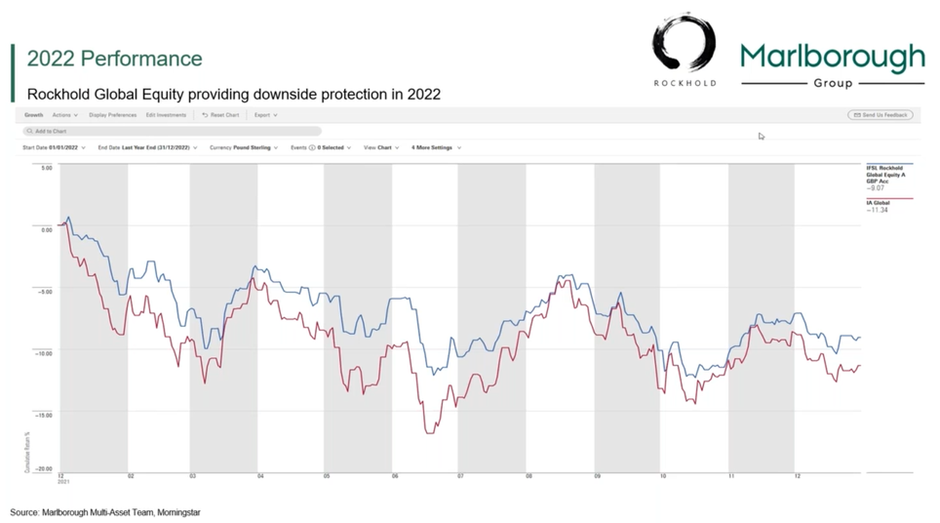

Rockhold launched these products at the back end of 2021, a pretty terrible time to launch a fund. As we've now witnessed 2022 was one of the worst equity market returns we've had on record, but what we can say is that we did a very good job of positioning the portfolio's defensively.

As you can see, the red line is showing you the performance of the IA Global and outperforming that is just demonstrating downside protection. The way we did that was by investing in funds which have an income focus, so sensible companies, UK equities, we were overweight the UK, we were short duration, and you can see that in the fixed income side, as well, providing downside protection.

So, both of those portfolios, which means that if you're constructing risk profile portfolios using the fixed income on the equity, you'll have delivered our performance last year.

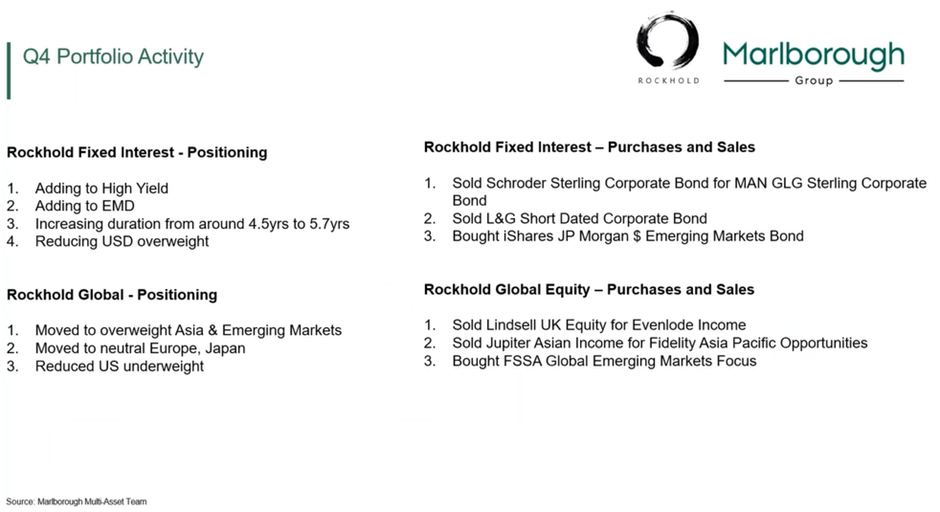

What have we been doing? The investment environment has changed for fixed income because I can now get a higher level of income because interest rates have gone up so high yields looks attractive, emerging market debt looks attractive, interest rates are less scary. So, we can add some duration.

The dollar tends to strengthen in a period of market stress that stress is now moving away. So the data is weakening meaning we're reducing that overweight to the dollar and you can see some of the things that we've done in portfolios as well.

On the fixed income side, we've sold the Australian corporate bond funds. The reason we did that is because the manager left and went to Man GLG. So, we looked at it, we met him, we looked at performance of Man GLG’s excellence and there’s good performance coming through there.

We then have sold some short duration, so I talked about the fact that we're adding to duration. So, you can see that I talked about the fact we're adding EMD, so we bought that. Then on the equity side, you can see some of the moves were going through there and recently, we are moving overweight Asia and Emerging Markets so we've been adding to that, brought in some new funds, moving to neutral and Europe and Japan and reducing the underweights to the US. You can see the moves there are telling you that we're more optimistic.

Lindsell train, we sold our fund and added even lower income, which is just because of superior performance. We sold Jupiter Asian Income, so this is a fund that it really well last year, good protection in an environment where we were concerned about Asia as a region. China's in lockdown global growth is slowing, that'll impact China, that region. That dynamic is changing, lets sell that fund, we don't need that anymore. Let’s buy Fidelity Asia Pacific, which has a higher weighting to China that so that Jupiter Asian Income has very little exposure to China. That was the reason behind that.

It’s worth reiterating some of those points there, particularly with fixed interest front. In the region of 1%- 2%, I've seen the same forecast, is now forecasting forward 5%- 6%, so that helps put the whole fixed interest in environment, in perspective.

Turning to the equities, if you start off the presentation with a line, each region is different. And let's look at some global asset allocation. We've got a big dispersion in valuations, particularly the US. Now, that's always been the case and there's always been a gap between the US and the rest of the world, it is the biggest market in the, world Index.

How do you, how do you view the US in from an asset allocation perspective, given its seemingly high relative valuation to its history? If we look at evaluate equations in the US, they always tend to trade at a premium to other regions. So, the question is, why is that? If you look at the return on invested capital, how much money you get from investing in the US, in a company? It tends to be double that, of any other region. So, the companies are basically generating higher profits, then, companies, in other regions. Why is that? Because they have such a big tech sector.

As we know, tech is a huge proportion of the benchmark. It was higher, so obviously tech share prices have come up, but it's about 20% - 25% of the S&P 500. That is really the reason. The key question going forward is, will higher interest rates impact that profitability? Are we at a point, let's call it a sea change, is this an environment where actually, the environment changes dramatically?

To give an example, if you think about the financial crisis, what happened after the financial crisis is central banks lowered interest rates to zero and then we had a sea change. We're now in an environment of super low debt. Now that we have interest rates moving back up 2%,3%,4%, does that present a new environment?

Now we’ve only got to be able to answer that question when we see will central banks have to drop rates back lower, back to where we were, or is this a new dynamic? If it's a new world, it just means that the profitability that those companies were generating will be lower, because their cost of financing will be higher. And the other thing I would say is that a lot of the edge that the tech companies had in the US is now proliferating into other industries.

Other industries are now hiring these tech people from the big companies and saying, how can we use you in our industry? How can we bring technology into industrials? How can we bring technology into car manufacturing? that's happening, you can see that. It just means that the playing field levels out a bit, and that takes some of the edge away from the US, However, I wouldn't write it off. But I do think that there's opportunities in other regions today, relative to the US. The US has its place on the global stage, but our preference today is to look at Emerging Markets and Asia, because of this and significant outperformance because of Covid, they've been restricted for three years. So, you should expect higher growth in China this year obviously, clearly, relative to the US and much higher. Therefore, that that's where we're leaning towards this year.

Important Information

The content of the blog is an extract of a presentation delivered to professional financial advisers only. It is not intended for or written for retail consumers. The information is for information purposes only and does not contain all the information needed to make any investment decision. Please seek professional financial advice before entering into or making an investment decision.

Investments carry risk. The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested.